7 Situations Where You Should Avoid Using Your Debit Card

Image Credit: Pille Kirsi/Pexels

Making payments has never been easier with the convenience of debit cards. They offer a quick, direct method to access funds and manage everyday expenses. However, it’s important to understand that these seemingly innocent plastic cards can present risks in certain situations. With around 70% of American adults regularly using debit cards, many are unaware of the potential drawbacks of relying solely on them for all transactions.

The growing threat of fraud, identity theft, and lack of adequate protection with debit card use can lead to unexpected headaches, especially when purchasing high-ticket items, booking travel, or handling online orders. Data from the Federal Reserve shows that over 25 million people fall victim to fraud each year, and debit card users often face financial repercussions more quickly than credit card holders.

Knowing when to choose a credit card over a debit card can make all the difference in safeguarding your financial security. Certain transactions, particularly those involving large sums, recurring payments, or online shopping, carry risks that a debit card simply can’t mitigate as effectively as a credit card can. Understanding the nuances of debit card limitations and credit card advantages ensures a safer, smoother financial experience in an increasingly digital world.

Online Shopping

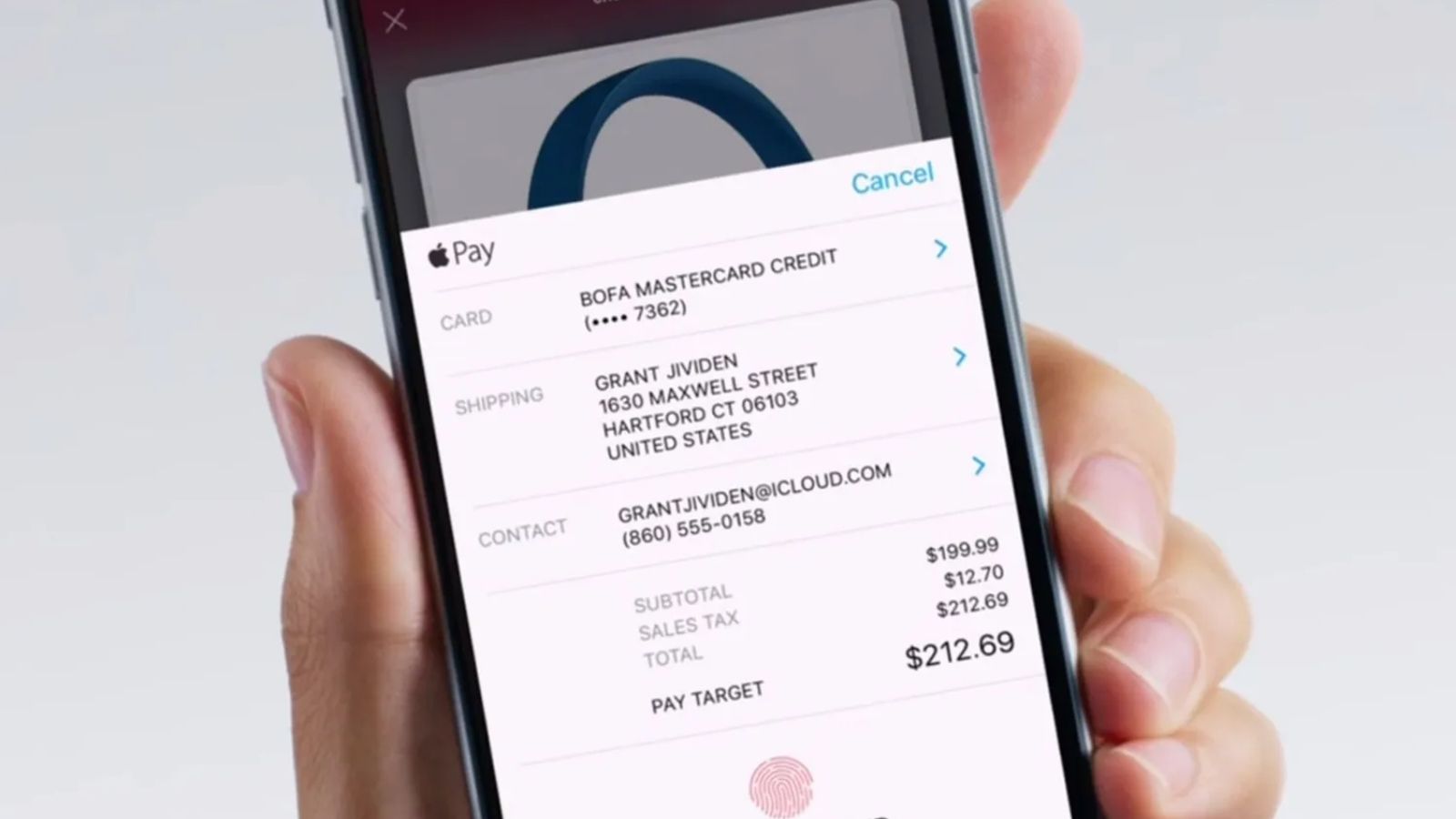

One of the most tempting ways to use a debit card is when shopping online. But the reality is that your debit card may expose you to risks. Since debit cards are linked directly to your checking account, unauthorized charges can quickly drain your balance. Unlike credit cards, which offer stronger fraud protections, debit cards leave you vulnerable if your information is compromised.

If someone steals your debit card details, the money is often taken from your checking account immediately, and getting it back can be a long, tedious process. A credit card provides more robust consumer protections. If there’s any issue with the transaction or if your card number is stolen, credit cards often limit your liability to $0, provided you report the fraud within the necessary timeframe.

Therefore, for safer online shopping, it’s recommended to use a credit card, which offers better fraud protection and greater recourse in case of disputes.

Big-Ticket Purchases

Whether you’re purchasing an expensive gadget, a car, or high-end electronics, it’s better to use a credit card than a debit card. Why? Because credit cards offer better dispute rights. If something goes wrong with the purchase—such as receiving damaged goods or no goods at all—you can dispute the charge with your credit card company and potentially get a refund.

In addition to dispute rights, many credit cards offer extended warranties and other perks for big-ticket purchases, such as travel or rental car insurance. These benefits provide added security for your large purchases. If you use a debit card, you may not have access to these protections, and the money will be withdrawn directly from your bank account, leaving you at risk if issues arise.

Deposits

When making purchases that require a deposit—whether renting equipment, booking a hotel room, or reserving a car—using your debit card might not be the smartest choice. While a credit card still places a hold for the deposit, it doesn’t directly affect your bank balance. Debit card transactions, on the other hand, can freeze significant amounts of your checking account funds as a deposit.

Using a credit card allows you to hold the deposit on the card without it affecting your available funds in your checking account. If the deposit is refunded, the money is returned to your credit card account rather than your checking account, which offers less risk and more flexibility.

Dining Out

Dining at a restaurant is a common place to use your debit card, but you should be cautious. When you hand over your card to a waiter, it’s out of your sight, leaving it vulnerable to skimming devices. Criminals can use handheld skimmers to collect your card details while the server is away from the table.

Debit cards are much more vulnerable to fraud because they are tied directly to your bank account, and any fraudulent transactions can drain your funds quickly. Credit cards, in contrast, offer more robust fraud protection. If fraud occurs, your credit card issuer can work with you to resolve the issue and limit your liability. Using a credit card while dining out helps reduce the risk of identity theft and fraud, making it the safer option.

First-Time Purchases

When dealing with a new company, especially one you haven’t bought from before, using your debit card might be risky. If a new business doesn’t meet expectations or delivers subpar products, it can be challenging to recover your money if you used a debit card.

Credit cards offer greater protection for first-time purchases, allowing you to dispute charges or even reverse them if necessary. Before you trust a new business with access to your checking account, consider using a credit card to safeguard your financial information.

Pre-Orders and Future Deliveries

For products you won’t receive immediately—whether it’s an upcoming fashion collection or an appliance that takes weeks to ship—a debit card may not be your best option. In case the delivery is delayed, damaged, or even never arrives, credit cards provide better protections than debit cards.

Credit card issuers often provide purchase protection, meaning you can dispute charges and request refunds if something goes wrong with your order. In contrast, using a debit card offers less recourse if things go awry. If your debit card is charged, the funds are immediately deducted from your checking account, leaving you with less protection to resolve the issue.

Subscriptions and Recurring Payments

Recurring payments like gym memberships, magazine subscriptions, or streaming services are common in today’s digital world. While these payments might seem like a convenient use for your debit card, they could create problems down the line. If you forget about a recurring charge or miscalculate your bank balance, your debit card may be declined, or worse, you might incur overdraft fees.

Credit cards offer more flexibility, allowing you to manage your recurring payments better and without draining your checking account. Furthermore, many credit card companies provide alerts and tools to help you track your payments, reducing the risk of forgotten subscriptions.

Conclusion

While debit cards are undeniably convenient, they come with a set of risks that credit cards can better mitigate. Whether you’re shopping online, booking a big-ticket item, or simply dining out, knowing when to use your debit card and when to opt for a credit card can help safeguard your financial security.

Credit cards provide stronger fraud protection, dispute rights, and additional benefits that can be valuable in specific situations. The key is to make informed decisions about how you handle your financial transactions. Consider the protection, benefits, and flexibility a credit card offers before making a purchase, especially when you’re making large transactions, booking services in advance, or dealing with unfamiliar companies.

By using your credit card in these 7 situations, you’ll keep your funds secure and enjoy peace of mind.